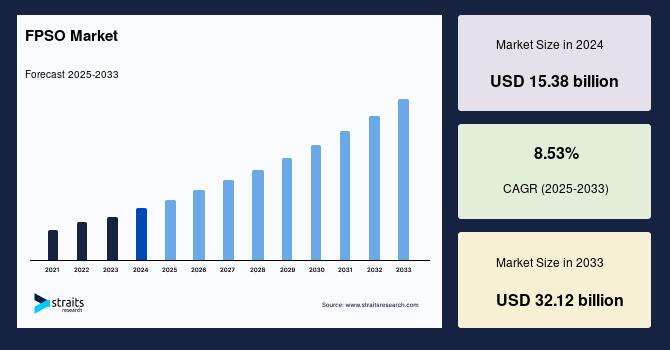

The global FPSO market size was valued at USD 15.38 billion in 2024 and is estimated to grow from USD 16.69 billion in 2025 to reach USD 32.12 billion by 2033 , growing at a CAGR of 8.53% during the forecast period (2025–2033).

Market Drivers and Trends Shaping Growth

Key drivers powering the global FPSO market include:

-

Rising Offshore Oil and Gas Exploration: With conventional onshore fields maturing, energy companies increasingly target offshore resources, particularly in deepwater and ultra-deepwater basins. FPSOs are ideally suited for these environments, supporting both production and storage efficiently.

-

Technological Advancements: Innovations in FPSO design such as modular construction, hull conversion technologies, and enhanced safety features like double-hull designs have improved deployment efficiency, operational reliability, and environmental compliance. Modular FPSOs reduce construction complexity and costs while allowing for faster project turnaround.

-

Energy Demand and Resource Access: Growing global demand for crude oil and natural gas, especially in emerging economies and regions like Asia-Pacific, drives FPSO adoption. Countries like Brazil, Malaysia, and Indonesia are expanding their offshore exploration activities, increasing FPSO deployments.

-

Flexible Ownership Models: Contractor-owned FPSOs have gained prevalence, enabling operators to reduce upfront capital expenditures by leasing FPSO units. This model supports financial flexibility and risk management in capital-intensive offshore projects.

Regional Market Insights

Among global regions, South America remains dominant, driven primarily by Brazil’s extensive offshore reserves in its pre-salt fields. Petrobras, Brazil’s national oil company, leads FPSO deployment here, fueling the region’s market leadership. The Asia-Pacific region is poised for fast growth due to rising offshore production in countries like Malaysia and Indonesia, aligning with expanding industrial energy needs.

The United States Gulf of Mexicoalso maintains a strong FPSO presence, supported by established operators such as ExxonMobil and Chevron focusing on deepwater fields. Emerging markets like South Africa are increasingly investing in offshore capabilities, contributing to the broadening geographical landscape of FPSO demand.

Segment Analysis and Market Structure

The FPSO market is segmented based on water depth, hull type, mooring systems, and construction method:

-

The ultra-deepwater segment predicts strong growth as exploration moves to deeper offshore areas exceeding 1,500 meters. These FPSOs enable access to vast untapped reserves previously inaccessible due to technological and economic constraints.

-

Double hull FPSOs dominate due to heightened environmental regulations and safety standards. This design mitigates oil spill risks and withstands harsh offshore conditions, ensuring compliance with global safety mandates.

-

In terms of mooring, spread mooring systems are more widely used, providing reliable positioning for FPSOs in various sea conditions. Meanwhile, FPSOs are increasingly developed using modular or converted vessels approaches to optimize cost-efficiency and deployment times.

Challenges and Restraints

Despite robust growth prospects, the FPSO market faces significant challenges, including:

-

High Capital and Operational Costs: Building and maintaining FPSOs require substantial investment, often reaching billions of dollars. Maintenance and compliance with safety and environmental regulations add to the ongoing financial burdens.

-

Economic and Oil Price Volatility: Fluctuations in global oil prices impact project approvals and operator investments, sometimes delaying market expansion.

-

Complex Regulatory Landscape: Offshore operations are subject to stringent safety, environmental, and operational regulations worldwide, requiring continuous innovation and compliance efforts.

Opportunities and Future Outlook

Collaborations through international partnerships and public-private alliances are emerging as vital opportunities in the FPSO space. These collaborations enable risk sharing, technology exchange, and capital pooling, which are essential for large-scale offshore projects.

Technological innovations such as automation, digitalization, and environmental performance monitoring (including greenhouse gas and methane emission tracking) are expected to drive efficiency and sustainability improvements in FPSO operations.

Looking ahead, the FPSO market's outlook remains highly promising due to persistent global energy demand, offshore resource potential, and continuous advancement in FPSO design and functionality. The sector's ability to adapt to environmental standards while unlocking remote reserves positions it as a cornerstone of offshore hydrocarbon production for decades to come.