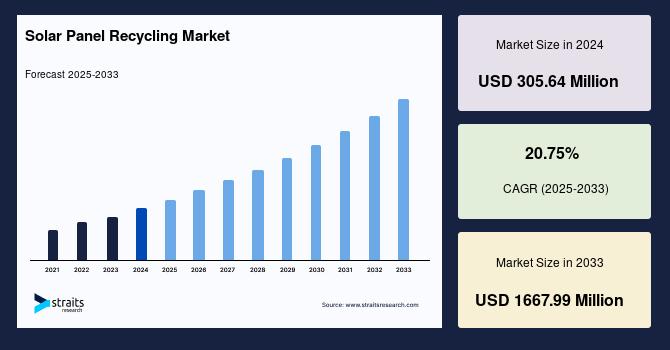

The global solar panel recycling market size was valued at USD 305.64 million in 2024 and is projected to grow from USD 369.06 million in 2025 to reach USD 1667.99 million by 2033, growing at a CAGR of 20.75% during the forecast period (2025–2033).

Why Is Solar Panel Recycling Gaining Urgency?

The surge in solar panel recycling demand stems largely from the rapid increase in solar photovoltaic (PV) installations globally. Countries worldwide are aggressively deploying solar power as part of their renewable energy strategies aimed at combating climate change and reducing carbon emissions. As these panels reach the end of their typical 25 to 30-year lifespan, massive volumes of solar panel waste are accumulating, posing environmental hazards if not managed properly. Hence, efficient recycling processes are vital to avoid toxic waste buildup and to support resource sustainability.

Complementing this environmental imperative is a trend of rising raw material costs and scarcity, particularly for elements like silver, silicon, and indium, which are critical in solar panel manufacturing. Recycling these materials from decommissioned panels offers a lucrative alternative to mining, helping stabilize supply chains in an industry increasingly mindful of resource constraints.

Drivers and Market Opportunities

A key growth driver in the solar panel recycling market is the enforcement of stringent environmental regulations and extended producer responsibility (EPR) policies. Regions such as the European Union have enacted comprehensive directives that mandate the responsible disposal and recycling of photovoltaic modules. These legislative frameworks not only compel manufacturers and importers to ensure proper end-of-life management but also incentivize investments in advanced recycling infrastructure.

Government incentives and subsidies further stimulate market growth by lowering the financial barriers associated with recycling operations. Alongside regulatory and policy support, technological advancements in recycling methods are enabling higher recovery rates of valuable materials while minimizing environmental footprints. Innovations in mechanical, thermal, and chemical recycling techniques improve efficiency and reduce costs, thereby enhancing the commercial viability of recycling solutions.

One of the most promising opportunities lies in strategic collaborations between solar panel manufacturers and recycling companies. These partnerships focus on creating closed-loop systems, where materials recovered from recycled panels are reintegrated into new production cycles. Such collaboration aligns with corporate sustainability goals and circular economy principles, ensuring both environmental benefits and supply chain resilience.

Regional Market Insights

Geographically, Europe currently leads the solar panel recycling market, propelled by mature environmental legislation, robust recycling infrastructure, and strong consumer awareness of sustainability issues. The region benefits from well-established extended producer responsibility programs and ongoing public-private initiatives that foster recycling innovation and effective material recovery.

Asia Pacific represents the fastest-growing market, fueled by its massive installed solar PV base and escalating solar waste challenges. Countries in this region are adopting emerging regulations to address environmental impacts, while their significant manufacturing capabilities underpin integrated recycling models that seek to reclaim valuable resources efficiently. Government-led initiatives and increasing technological adoption are rapidly expanding the solar panel recycling infrastructure here.

North America also shows significant market momentum, supported by rising concerns about solar waste management, regulatory emphasis on electronic waste, and substantial solar infrastructure investments. The region’s advanced technological capabilities and commitment to circular economy strategies help in developing specialized recycling systems, promoting sustainable solar energy lifecycles.

Market Segmentation and Technology Trends

Monocrystalline solar panels dominate the recycling market. Their extensive use in residential and commercial installations, coupled with their high silicon purity, makes them highly attractive for recycling. As earlier generations of these panels reach end-of-life, the volume of recyclable monocrystalline panels is increasing quickly.

Mechanical recycling is the predominant method in the market due to its cost-effectiveness and operational simplicity. This process involves crushing, shredding, and separating materials such as glass, silicon, and metals with minimal chemical usage, making it environmentally favorable and widely deployable. Mechanical techniques excel particularly in processing crystalline silicon panels, which constitute the majority of solar waste, and their scalability supports the growing volumes of end-of-life panels.

Metals form the dominant category of recovered material in the solar panel recycling market. Panels contain valuable metals like silver, aluminum, and copper essential for electrical conduction and support structures. Recovering these metals not only addresses raw material shortages but also significantly lowers the environmental impact compared to virgin mining. The high resale value of these metals solidifies their importance in the recycling ecosystem.

Challenges and Market Restraints

The solar panel recycling market faces notable hurdles. The recycling process is complex and costly, involving multiple steps such as dismantling panels, separating intricate materials, and purifying recovered substances. Advanced technologies and skilled labor are required, leading to high operational expenses.

Furthermore, the economic returns from recycling are currently limited compared to costs, partly due to the lack of standardized recycling procedures for different panel types, including crystalline silicon and thin-film panels. These limitations hamper widespread adoption, especially in regions lacking strong recycling infrastructure or supportive policies.

Additionally, technological constraints limit the efficiency of extracting high-value materials like silicon wafers and silver. Current processes may degrade these materials, reducing their usability and profit margins, thus deterring investments in large-scale recycling operations.

Industry Outlook and Key Players

The rising volume of solar panel waste presents both a challenge and a significant market opportunity. Companies in this sector are expanding processing capacities by investing in technological innovation and forming strategic partnerships with manufacturers and governments. Efforts focus on developing cost-effective recycling methods that maximize material recovery while aligning with environmental and corporate social responsibility standards.

Prominent players like Canadian Solar exemplify commitment to sustainability by integrating recycled materials into their production cycles and investing in recycling technologies to bolster the circular solar economy.

Looking forward, the solar panel recycling market is poised for robust growth, driven by regulatory pressure, increasing solar waste volumes, resource scarcity, and improved recycling technologies. As the industry evolves, recycling will become an indispensable component in the global solar energy value chain, supporting environmental sustainability and resource conservation.