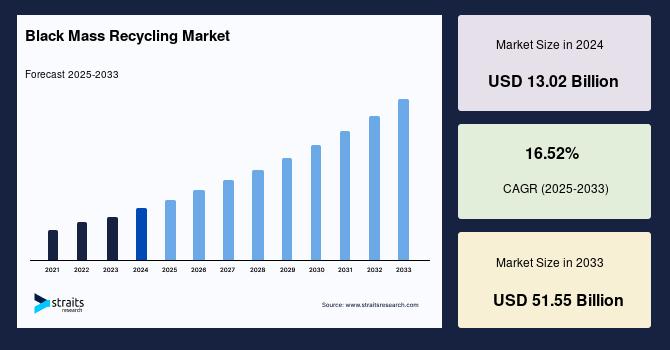

The global black mass recycling market size was valued at USD 13.02 billion in 2024 and is projected to grow from USD 15.17 billion in 2025 to reach USD 51.55 billion by 2033, growing at a CAGR of 16.52% during the forecast period (2025–2033).

What is Black Mass Recycling and Why Does It Matter?

Black mass is a material derived from the recycling of spent lithium-ion batteries and manufacturing scrap. It contains concentrated amounts of valuable metals essential for battery production. The recycling process involves collection, dismantling, crushing, and then extracting these metals through advanced techniques like hydrometallurgy. Recovering metals from black mass reduces the reliance on virgin mining, which is often environmentally harmful and geopolitically uncertain, thus fostering a more sustainable and resilient supply chain for the battery and EV industries.

Market Growth Drivers

The principal factor accelerating the black mass recycling market is the surging adoption of electric vehicles worldwide. Global EV sales have increased dramatically in recent years as governments and industries seek to reduce carbon emissions and address climate change. As EV batteries reach their end of life, volumes of spent lithium-ion batteries and consequently black mass are rising sharply, creating a steady and economically viable feedstock for recyclers.

In tandem with market demand are stringent environmental regulations and policies incentivizing battery recycling. Regions like the European Union have introduced extended producer responsibility (EPR) mandates requiring battery manufacturers to ensure material recovery and reuse. North America and China have also committed significant investments to build domestic recycling capacities, aiming to secure supply chains and reduce import dependencies.

Another key driver is the shift toward circular economy principles by battery manufacturers and recyclers. There is growing collaboration across the value chain to develop closed-loop systems where recovered metals re-enter battery production, lowering carbon footprints and enhancing resource efficiency.

Technology and Process Innovations

Hydrometallurgical processes are taking precedence in black mass recycling due to their high recovery rates and lower environmental impact compared to traditional pyrometallurgical methods. This process uses aqueous chemical solutions to selectively leach and extract metals such as lithium, nickel, cobalt, and manganese from black mass efficiently.

Technological advancements also address challenges like variable battery chemistry, contamination, and energy consumption. Companies are deploying automation, AI-driven process controls, real-time impurity sensors, and solvent-extraction technologies to improve yield and reduce costs. The ongoing R&D emphasizes scaling up operations while minimizing environmental impact.

Regional Market Insights

Asia-Pacific dominates the global market, propelled by its significant EV manufacturing bases, established battery supply chains, and government initiatives promoting battery waste management and recycling infrastructure. The region benefits from relatively lower labor costs and technological advances that facilitate large-scale deployment of recycling plants.

North America is the fastest-growing market segment, boosted by increased domestic battery production, supportive regulations including tax incentives, and strategic partnerships between recyclers and automakers. The U.S., in particular, is investing heavily in developing closed-loop battery material supply chains, reflecting its shift toward electrification in transportation.

Europe also shows strong growth prospects due to aggressive environmental policies, decarbonization targets, and robust regulatory frameworks mandating recycled content in new batteries. Public-private collaborations foster innovation in green recycling technologies and the formation of regional recycling hubs aimed at reducing dependency on imports.

Challenges and Market Restraints

Despite the promising outlook, the market faces several challenges. High operational costs remain a significant barrier, driven by energy-intensive processing, specialized equipment, and stringent safety and environmental compliance requirements. Many developing regions lack adequate infrastructure and skilled labor, limiting widespread adoption of black mass recycling.

Additionally, the diversity and evolving nature of lithium-ion battery chemistries complicate standardization of recycling processes, affecting recovery efficiency and increasing the risk of contamination.

Key Metals and End-Use Trends

Nickel is a particularly valuable metal recovered from black mass due to its importance in enhancing battery energy density and performance. Demand for nickel-rich cathode chemistries in EVs supports strong growth in nickel recycling. Lithium, cobalt, and manganese likewise constitute critical recovery targets because of their high demand and supply constraints.

Automotive batteries generate the largest share of black mass due to the rapid growth of electric vehicle fleets and the relatively short replacement cycle of EV batteries. Electronic devices and energy storage systems are also prominent contributors to black mass feedstock.

Industry Developments and Outlook

Leading players in the black mass recycling market are expanding capacity, refining recycling technologies, and often partnering with battery makers and automakers to secure feedstock and create integrated circular supply chains. Companies like Ecobat Technologies have established multiple advanced recycling facilities capable of substantial black mass production, with plans to scale further.

With the global push for sustainability and electric mobility, black mass recycling is poised to become a cornerstone of the battery materials supply chain. Continuous technological innovation, policy support, and strategic collaborations will be critical to overcoming cost and operational challenges, enabling this market to sustain its high growth trajectory through the next decade.