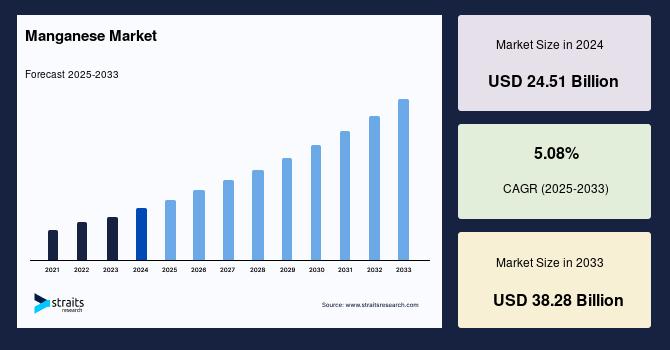

The global manganese market size was valued at USD 24.51 billion in 2024 and is projected to grow from USD 25.76 billion in 2025 to reach USD 38.28 billion by 2033, growing at a CAGR of 5.08% during the forecast period (2025–2033).

What Is Propelling the Manganese Market Growth?

Manganese is a vital metal primarily used in steel manufacturing to enhance durability, hardness, and corrosion resistance. As global infrastructure and automotive demand rise, especially in fast-developing regions of the Asia-Pacific, manganese consumption keeps pace. The metal’s strategic importance is underscored by its inclusion as a key alloying element in steel for bridges, pipelines, rail tracks, and automotive components.

The growing electric vehicle industry and energy storage systems represent a fast-expanding market segment for battery-grade manganese. High-purity manganese sulfate and electrolytic manganese metal are increasingly critical materials in the production of lithium-ion batteries with nickel-manganese-cobalt (NMC) and related cathode chemistries. Efforts by countries such as the U.S. and European nations to secure local manganese supply chains and develop refining capacity are key trends supporting this demand surge.

In addition to these core sectors, manganese-based fertilizers play an important role in agriculture, boosting nutrient supply for staple crops like soybean, wheat, and corn. Chemical and ceramic industries also contribute to market demand, utilizing manganese compounds in applications ranging from glass manufacturing to water treatment.

How Are Supply Chains and Technological Innovations Impacting the Market?

Manganese mining and refining remain concentrated in a handful of countries, with South Africa, Australia, and Gabon accounting for the majority of global supply. This geographic concentration introduces risks, including political instability, labor disputes, export regulation changes, and logistical challenges like port congestion and rising freight costs. These factors contribute to price volatility and supply chain unpredictability, particularly for battery-grade materials.

Nonetheless, mining companies and governments are investing to expand and diversify production capacities, aiming to mitigate these risks. Technological advances enable improved extraction from lower-grade ores and processing of tailings, boosting resource efficiency and sustainability. Clean energy initiatives also drive efforts to lower the environmental impact of manganese production, including the adoption of greener refining technologies.

Battery-grade manganese production is a focal point of innovation, as demand grows for stable and high-quality materials to meet EV battery specifications. Regional plans to cultivate domestic supply chains seek to reduce import dependency and promote energy security.

What Regional Trends Are Shaping the Market Landscape?

Asia-Pacific dominates the manganese market, propelled by its leading steel production volumes and rapid urbanization in China, India, and Southeast Asia. The region’s infrastructure projects, expanding automotive industries, and rising consumption of consumer electronics drive manganese demand for both steel alloys and batteries. Availability of rich manganese reserves, along with investments in mining infrastructure and processing technology, solidifies Asia-Pacific's market leadership.

North America is the fastest growing regional market, stimulated by government incentives favoring domestic battery production, clean energy transitions, and recycling technologies. Infrastructure modernization programs further boost manganese use in steel for transportation and construction sectors. Efforts to localize production of battery-grade manganese and reduce foreign dependency are key features of this market expansion.

Europe’s manganese market growth is driven by automotive and steel industry demand aligned with carbon neutrality and green mobility strategies. Increasing electric vehicle adoption fuels the need for high-purity manganese cathode materials. European countries are also advancing recycling and circular economy approaches, reclaiming manganese from end-of-life batteries and industrial waste.

What Are the Main Market Segments and Applications?

Steelmaking remains the largest application segment for manganese. The metal is essential for its role in deoxidizing steel and improving tensile strength, wear resistance, and durability. Demand is closely tied to industrial production, construction activity, and automotive output globally.

The battery-grade manganese segment, though smaller in volume, is experiencing the fastest growth rate due to soaring electric vehicle and energy storage battery production. High-purity manganese products such as electrolytic manganese metal (EMM) and manganese sulfate feed this thriving segment. Expansion of refining technologies enhances product quality and availability.

Agricultural fertilizers containing manganese contribute to market diversity, supporting nutrient balance and productivity for major crops. Chemical manufacturing, dry-cell batteries, glass, and ceramics utilize manganese compounds in various specialized applications, exemplifying its broad industrial relevance.

What Challenges and Opportunities Lie Ahead?

Key challenges for the manganese market include supply chain vulnerability attributable to geographic concentration of mining, price volatility, and environmental concerns around mining and refining practices. Companies are responding by diversifying production, enhancing recycling efforts, and adopting sustainable mining techniques to reduce ecological footprints.

Investments in research and development are fundamental to improving processing efficiency, environmental performance, and product quality—especially for battery-grade manganese. Strategic collaborations with electric vehicle and battery manufacturers are emerging to secure supply reliability.

Overall, the manganese market outlook is positive, supported by converging demand from traditional industrial uses and the accelerating green energy transition. As economies invest in infrastructure and clean energy technologies, manganese is positioned as an indispensable metal that bridges conventional manufacturing with emerging sustainable industries.